As slick as the Apple Card is, its features are unique only in their mix, presentation, and integration into iOS. Doing business elsewhere doesn’t mean you miss out on real-time fraud alerts, payment reminders, cash back and the like.

In fact, the majority of the Apple Card’s defining features have been around for ages, and odds are they’re available in a credit card you already possess. That’s particularly so if it was issued by one of large banks—Chase, American Express, Discover, Citibank, Capital One, or Bank of America.

Pitting those companies’ approaches against Apple’s doesn’t result in exact equivalents, of course. For example, while most credit cards from a single big bank come with the benefits we’ve outlined below, not every one does; you’ll need to verify the specific card you have or want has what you seek. Some features also require manual set up. And a handful of features can’t be replicated at all.

But having a choice beyond Apple means you can pick the right card for your personal finances. The Apple Card versus the competition isn’t a winner-takes-all scenario, as you’ll see.

Seeking specific credit card recommendations? We’ve made a list of the best Apple Card alternatives, with callouts for best overall, best for cash back, best for low-interest rates, and more.

Apple Card features you can get elsewhere

Cash-back rewards

You can get cash back as a reward with quite a few credit cards that have no annual fee. These cards vary in their approach. Some pay a flat rate for all purchases, with the best ranging between 1.5 to 2 percent. Others offer tiered rewards (like the Apple Card), where some categories of purchases qualify for different amounts of cash back. For example, the Discover it Cash Back doles out 5 percent on a rotating series of categories, and 1 percent on everything else, while the Citi Costco Anywhere Visa pays 4 percent on gas, 3 percent on travel and dining, 2 percent at Costco, and 1 percent on everything else.

Citibank

Citibank

The Citi Double Cash pays 2 percent on all purchases, unlike the Apple Card.

Some Apple Card fans have argued that the 3 percent back for Apple purchases can’t be beat. That’s true but not very relevant to most people, as they’ll spend greater amounts in areas like food, travel, and home improvements. The Apple Card won’t maximize rewards for them.

If you’re in the market for a new credit card anyway, a handful of the best come with sign-up bonuses or introductory bonus cash back, which can net juicy rewards that cancel out or exceed what you’d normally earn on an Apple Card. For example, the Wells Fargo Propel awards a $300 sign-up bonus if you spend $3,000 within 90 days. Buying Apple goods (say, a loaded MacBook) on the non-Apple Card is the smarter move, as you’d have to spend $10,000 on Apple products or services on an Apple Card to match that amount.

We name specific recommendations for cash-back cards in our Best Apple Card alternatives article, plus compare the numbers on cash-back percentages, interest rates, and fees in our rundown of the Apple Card and its two nearest rivals.

Contactless payment

Apple

Apple

Because credit cards issued by major banks are compatible with Apple Pay, you won’t miss out on contactless payment as an option.

Skipping on an Apple Card actually can increase your options for contactless payment, since word on the street is that the physical version of the Apple Card won’t support it. The list of banks that support Apple Pay includes all the major credit card issuers we researched for this article, plus a good number of credit unions and smaller banks, too. On top of that, American Express, Capital One, Citibank, and Chase are all heavily pushing physical cards with tap-and-pay capabilities right now.

End-of-the-month payment due date

Does the due date for your credit card payment fall in an awkward part of the month? You can move it. All of the big banks let you pick your own, typically between the 1st and 28th of the month, provided your account is current. (In other words, you have no past-due payments.*) Most banks let you select the new date via their website, but if not, you can also do so with a phone call.

200degrees (CC0)

200degrees (CC0)

You can change your payment due date in minutes.

Why the date-range limitation, and why can’t your payment due dates fall on exactly the end of every month, like with the Apple Card? It’s likely because of a strict adherence to the CARD Act of 2009. The regulations say that due dates for credit card payments must be the same day each month, and by disallowing the 29th, 30th, or 31st as options, card issuers can follow that law to the letter. (Or perhaps keep their software systems from choking.)

The upshot of this system that you can change the date to any day within that period. Perhaps you don’t get paid on the 1st or the 15th, or there are other bills that fall at the end of the month you’d prefer to space out. You can accommodate those.

*Some credit card issuers have further restrictions on how soon you can change your due date and how often you can do it. You may need to wait past the first billing cycle for a new card, or past 90 days since the last adjustment. Also, be aware American Express does distinguish between its credit cards and its charge cards, and Wells Fargo has some oddly specific dates that are acceptable.

Low interest rates

Because the Apple Card only has the lowest interest rates for a rewards credit card, it’s not hard to beat it on this one point. For one, you’re not guaranteed its absolute best annual percentage rates (APR)—that’s determined by how creditworthy Apple and Goldman Sachs find you.

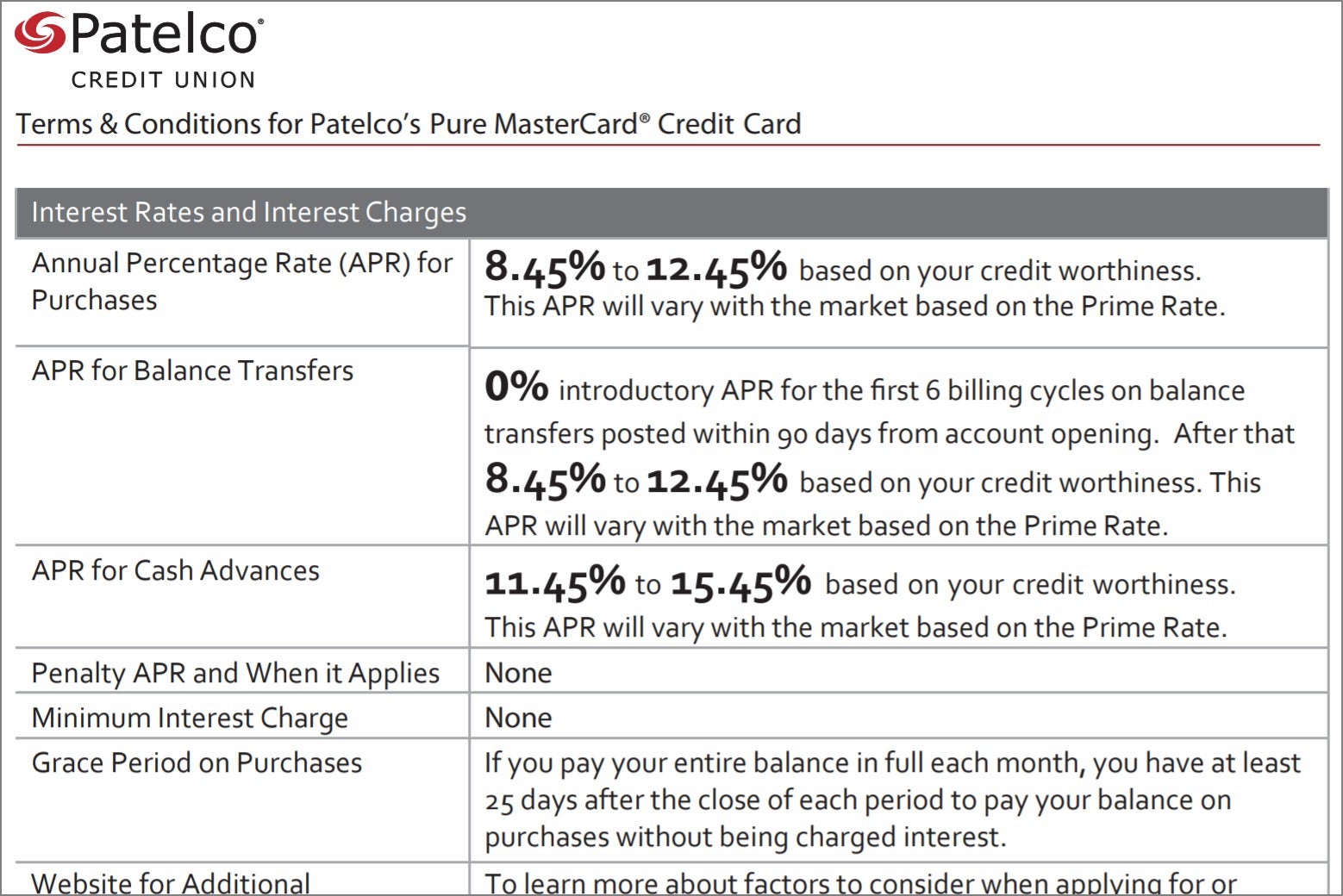

Patelco

Patelco

Credit unions are the best source for straightforward, low-interest-rate credit cards.

Second, even if you are saving 2 to 3 percent over other rewards cards, you’re still accruing interest at a rate that’s anywhere from 6 to 27 percent higher than the better alternatives. Whatever you earn in rewards won’t be enough to come out ahead.

You have two options for a low-interest rate credit card. The first is straightforward and easier to manage: a plain, no-rewards credit card with no annual fee. Credit unions are your best bet for this type of card, as their mission is to serve their members. They do so by offering lower interest rates on loans and credit cards, and higher rates on savings accounts and certificates-of-deposit. Currently you can find low-interest cards from select credit unions with rates starting as low as 7.25 percent.

A few credit unions actually offer rewards cards with interest rates this low, but finding such a card is based on luck of geography and your affiliations. Credit unions allow people to join based on where they work, live, worship, or if a relative is already a member.

The second option is a zero-interest credit card, which is suited solely for people who have excellent credit, a specific strategy around their debt, and the ability to pay it off quickly. These cards generally offer an introductory rate of 0 percent interest on new purchases and balance transfers for the first 12 to 18 months. If you go this route, look to avoid fees if transferring a balance, and eliminate your debt before normal interest rates kick in (anywhere from 16 to 26 percent).

Metal credit card

Metal cards similar to the Apple Card aren’t numerous, but if you drop further down the list of larger credit card issuers, you can find a slab of metal alloy with no annual fee and a tiered set of rewards.

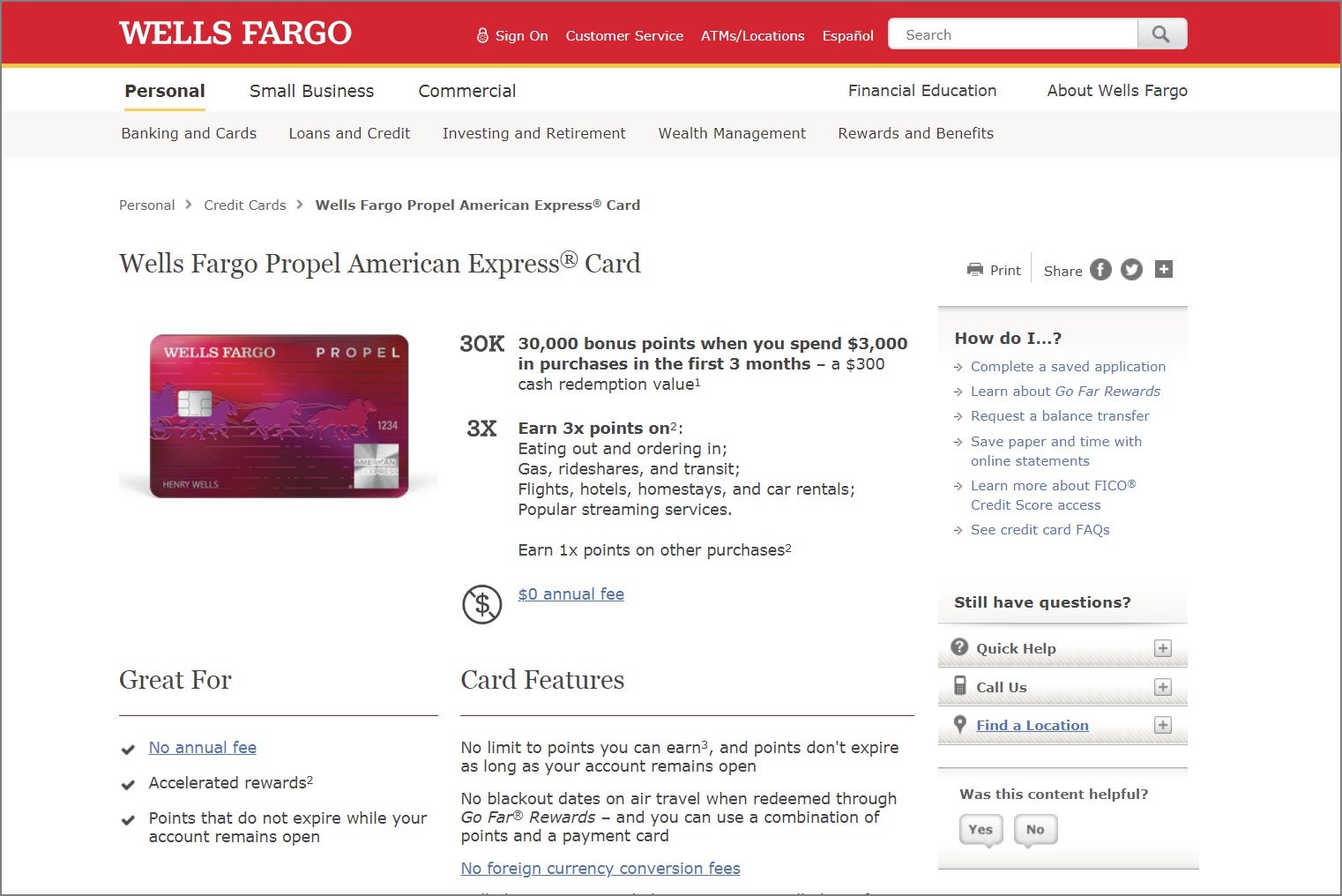

Wells Fargo

Wells Fargo

Like the Apple Card, Wells Fargo Propel American Express card is made of metal and has cash-back rewards.

The standout example is the Wells Fargo Propel, an American Express card that has no annual or foreign transaction fees, and up to 3 percent back on select categories. It’s not an ideal option for anyone planning to carry a balance from month-to-month though, as the interest rates are much higher than the Apple Card’s. (But as mentioned above, you really shouldn’t carry a balance on a rewards card anyway.)

Dedicated travelers have more choices, but going in that direction is a different strategy than with an Apple Card. To make the most out of a card like the Chase Sapphire Reserve or American Express Platinum, you must pay off your balance every month and dine out or travel with a certain frequency to overcome the hefty annual fees.

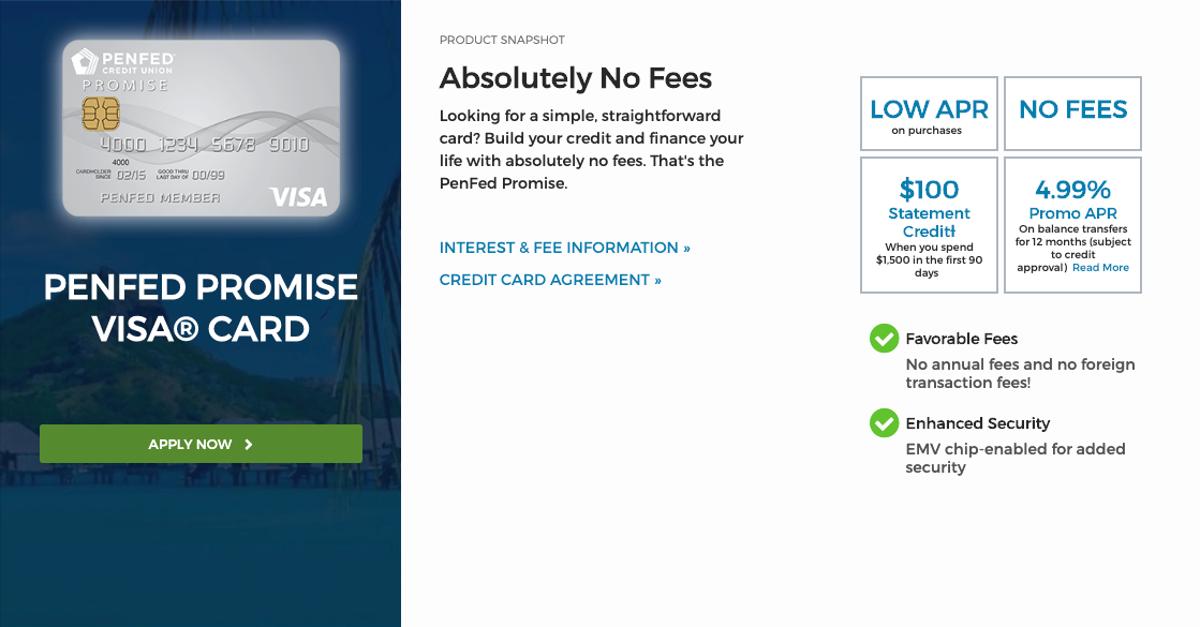

No fees

With an Apple Card, you completely avoid common fees like those of the annual, balance transfer, late payment, foreign transaction, cash advance, over the credit limit, and returned payment varieties. That’s a rarity, but not impossible to find elsewhere. You just need to sift through offerings from credit unions.

PenFed

PenFed

PenFed’s Promise Visa truly has zero fees.

Our searches uncovered one card available to everyone (provided that you can make a donation to charity if you’re non-military), Pentagon Federal Credit Union’s Promise Visa, and it’s possible that local credit unions in your area might have similar card. (Those near Macworld’s office are not completely fee-free, but the best have very few fees along with excellent benefits. The perks definitely vary from credit union to credit union.)

If you’re not able to avoid fees all together, you can and should avoid a few common ones. For starters, many good rewards cards don’t charge an annual fee. The best ones also don’t charge a foreign transaction fee, which is usually 1 to 3 percent of purchases made through a foreign merchant.*

As for late fees, you can typically request a waiver from customer service if you’re a customer who typically pays at least your monthly minimum due. Banks sometimes offer zero-fee balance transfers to select customers, as well. These options doesn’t remotely resemble the Apple Card, of course, but they do exist.

*Note: To avoid accidentally paying more for international purchases, always refuse being billed in U.S. dollars. The merchant’s bank will almost always use a worse conversion rate than your card’s network (Visa, Mastercard, etc.). This issue is separate than foreign transaction fees, so you’re not immune even with a card lacking fees.

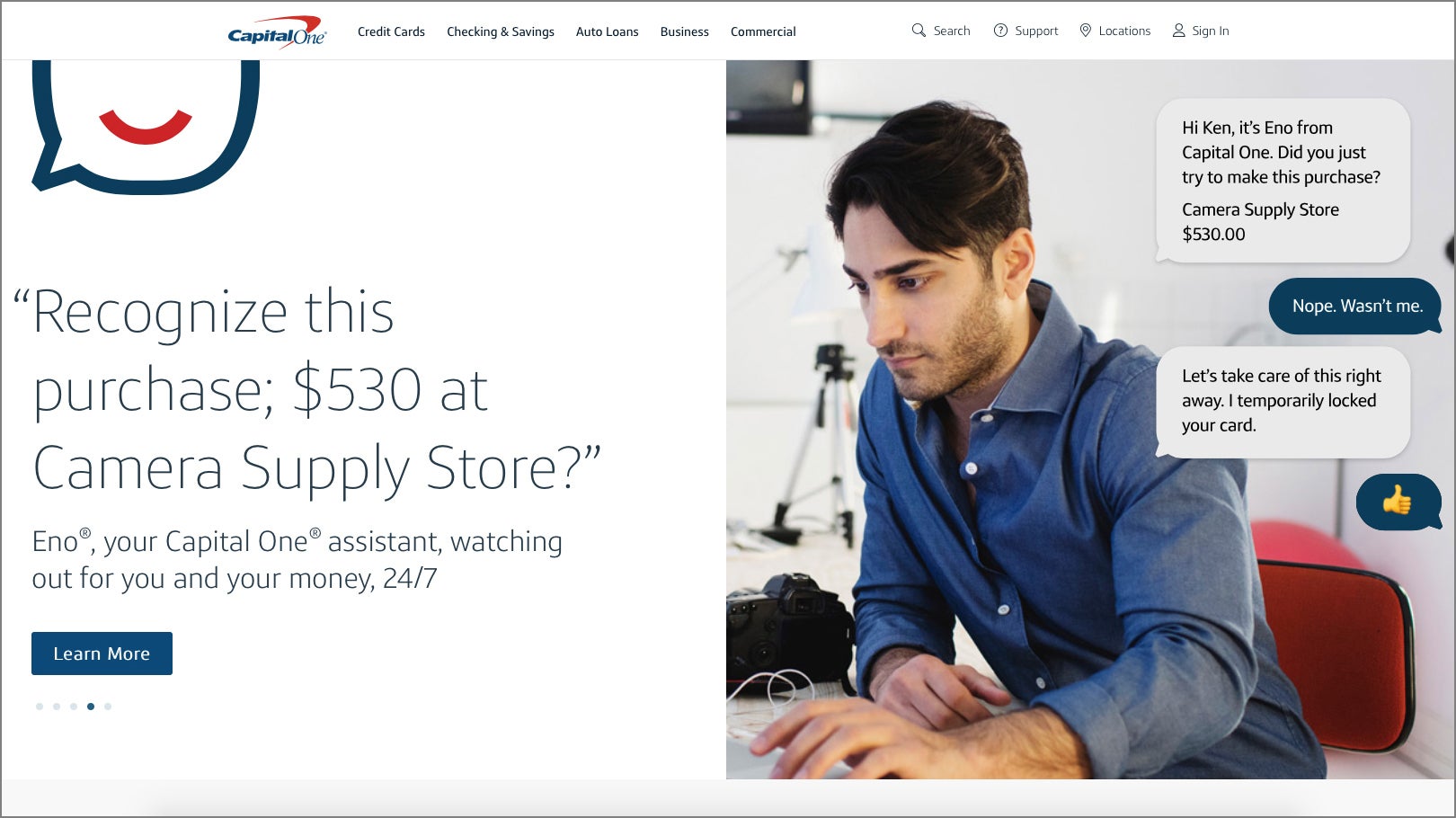

Real-time fraud alerts

Virtually every bank and credit union offers real-time fraud alerts via text message, email, or through its app. Most credit card issuers automatically set these to fire if any suspicious activity is detected, but you can confirm they’re active by logging into your account. (Look for “account alerts.”)

Capital One

Capital One

The Apple Card is not the lone credit card offering real-time fraud alerts.

When performing that double-check, you can also change your preferences for how alert are sent. Receiving messages through the app is slightly more secure than text messages, as the latter are vulnerable to hijacking (primarily through someone stealing your phone number and transferring it to a SIM card in their possession).

In addition to fraud alerts, which rely on algorithms based on your spending habits and general fraud trends, you can also manually set alerts for charges as a backup for catching suspicious activity. You can set these to trigger if a purchase exceeds a certain amount, and some issuers like Bank of America and Chase also let you set it based on location, such as a gas station or online. The exact options vary by institution.

Payment reminders (and other alerts)

All of the major credit card issuers let you set up text message, email, or app reminders for when your payments are due. The time frame for how soon you can be alerted varies between bank, but often it’s a customizable period.

You can also opt in to other alerts, like balance transfers, refunds, or charges over a certain amount. As mentioned above, real-time fraud alerts are usually active by default on accounts, but you can check on those from your account while logged in and customize them to suit your preferences.

The exact list of alerts varies slightly from bank to bank, with a few nuances particular to each one—for example, Bank of America lets you monitor online purchases made with your card. But overall, the approaches taken by the big card issuers mostly overlap.

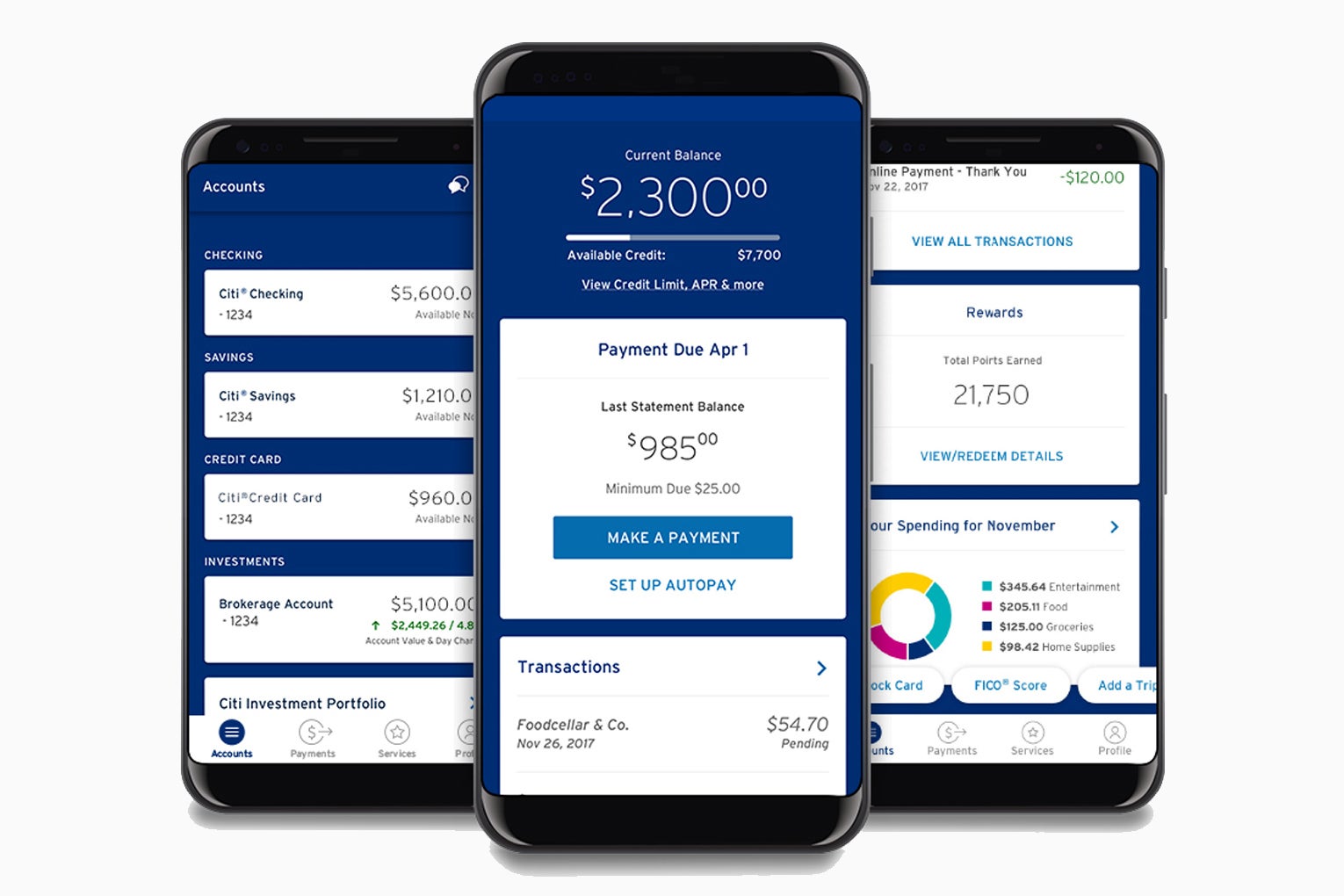

Spending reports

Citibank

Citibank

Citibank provides a categorized summary of your purchases, which you can access via a desktop computer or on mobile.

Colorful bar charts do make it easy to see where your money’s going. So it’s fortunate that other credit card issuers also break down your spending patterns. Most of the big banks give summaries of your purchases, along with color-coded categories and the ability to drill into each to see the individual transactions. The feature goes by different names at each institution—like Spend Analyzer or Trend Summary—so you may have to hunt a little while logged in to find the option.

Of the bunch, Citibank stands out for the ability to go beyond weekly and monthly summaries. You can choose custom time periods that let you see even just a few days’ worth of categorized purchases. Other card issuers provide a minimum of yearly intervals, with companies like American Express and Discover offering a better set of time spans that include a monthly summary as the shortest period.

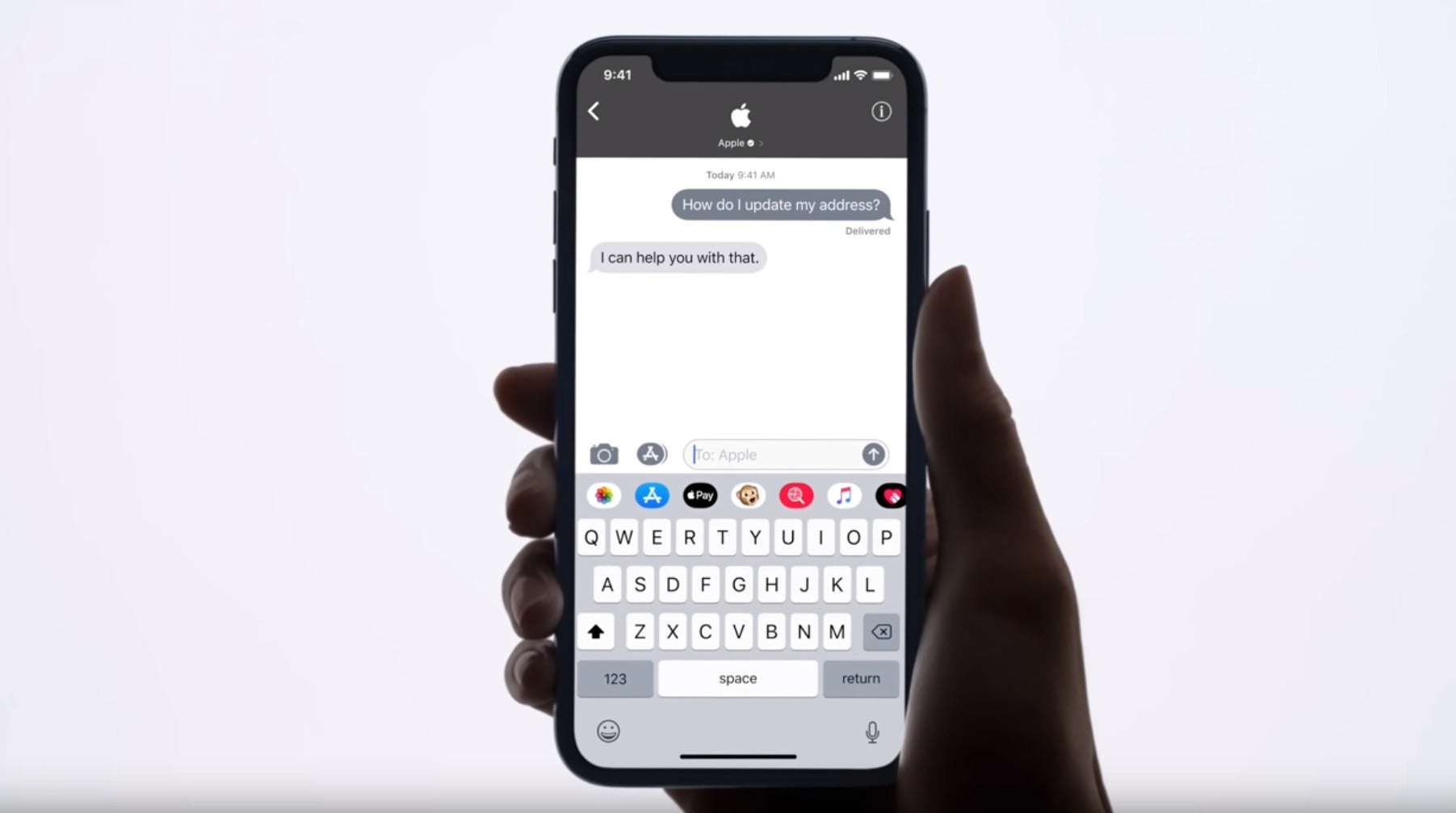

Text-based customer service

Apple

Apple

Discover and Wells Fargo also use Business Chat to communicate with customers, though Wells Fargo’s service is still in a pilot phase and unavailable in our area for us to try.

Apple’s real-time, text-based customer service is a boon for people who hate talking on the phone, much less wasting time listening to dreary hold music. You get the same level of service and security as you would by calling in, as it’s handled by live agents over Apple’s Business Chat feature in iMessage.

Most big card issuers rely on standard SMS text messages for limited, automated interaction, but two of them—Discover and Wells Fargo—also make use of Business Chat, opening up that same ease of communication to their customers. (Wells Fargo is still in a pilot phase, however, so this contact method is only available in supported locations.) When we tried out Discover’s service, it worked just as the Apple Card’s does. Responses were reasonably timely, with little back and forth before our question was answered.

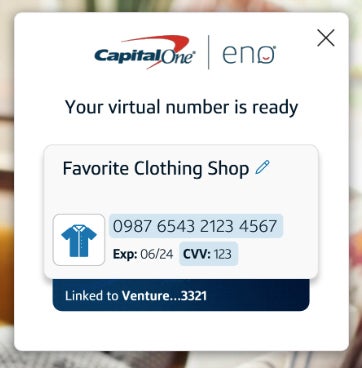

Virtual credit-card numbers

Virtual card numbers are a security benefit provided by both Apple and its some of its rivals, but their styles of implementation differ.

For the Apple Card, a virtual number protects you from fraud if your physical card goes missing. You only see it in the Wallet app, and only use it for purchases made online and over the phone. It’s separate from the physical card and how those transactions process.

Capital One

Capital One

Capital One and Citibank’s virtual card numbers are merchant-specific, which provides an added layer of protection if the number gets stolen or leaked.

This virtual number does not add any extra protection for digital and phone purchases. It remains constant until you decide to regenerate it through the app. If it changes, you will need to update your billing info with every business who charges you on a recurring basis (e.g., a cell phone provider). The process is the same as if you had to request a replacement physical card from a typical bank, but with fewer delays.

In contrast, Apple’s rivals on this front —Citibank, Capital One, and Bank of America—treat a virtual number as a random credit card number with a unique expiration date and CVV tied to your account. Its specific purpose is to provide privacy and security for shopping done online and over the phone. You can create more than one of these at a time through the bank’s website (or if available, an installed desktop application) and use them simultaneously, too.

Depending on the bank, these numbers can also be specific to the merchant they’re used with (Citibank, Capital One) and can have customizable expiration dates up to one year in the future (Bank of America, Citibank). Citibank also allows you to set a custom spending limit.

If you must replace your physical card with one that has a refreshed account number, you don’t need to make any updates involving your virtual numbers. You only have to update your billing info when the virtual number expires.

Next: Apple Card features you can’t get elsewhere

https://www.macworld.com/article/3431666/apple-card-features-you-can-get-elsewhere.html

2019-08-26 10:00:00Z

CAIiEEuua5riMDPL5zMMbbb1JIYqFAgEKg0IACoGCAowypIBMMAfMPhR

Bagikan Berita Ini

0 Response to "11 Apple Card features you can get elsewhere—and 4 you can’t - Macworld"

Post a Comment